💡What is Qualified Term (Qt)?

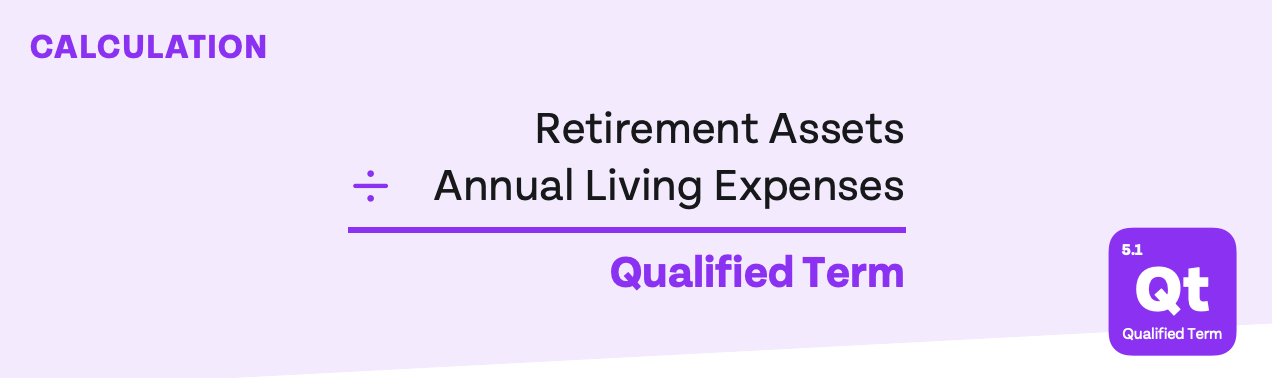

Qualified Term (Qt) represents the number of years you could sustain your current lifestyle on your existing qualified retirement assets, assuming neither your lifestyle nor your assets change. Qualified retirement assets are accounts that may be subject to a tax penalty upon early or nonqualified withdrawal.

These include:

- Roth and Traditional IRAs

- Roth and Traditional 401(k)s

- SIMPLE IRA

- SEP

- 529

- Profit Sharing Plans

- Defined Benefit Plans

- Health Savings Accounts (HSA)

- 403(b)s

- Annuities

- Minor Roth and Traditional IRAs

📚 Breaking It Down: Calculating Your Qt

To determine your Qt, divide your total retirement assets by your annual living expenses. For instance, if you have:

- $400,000 in your 401(k) + $100,000 in your Roth IRA + $10,000 in your HSA

- And spend $100,000 per year

- Your Qt would be 5.1 years.

Understanding your Qt helps assess your asset mix—the concentration of your wealth—and your utilization. In other words, it enables you to determine if you have too much or too little in retirement accounts relative to your overall net worth. Additionally, it allows you to evaluate whether you are maximizing the benefits available through your retirement accounts.

🔑 The Importance of Qt for CRNAs

A well-balanced Qt is crucial for several reasons. Typically, individuals who maximize their retirement plan contributions annually within the appropriate plan will experience lower tax liability and increased savings over their career. Moreover, people generally consider qualified retirement accounts to be earmarked for long-term objectives, resulting in more consistent long-term investment behaviors.

However, it’s essential to strike a balance between retirement accounts and liquid accounts. At times, you might need to prioritize building liquid assets over qualified retirement assets to maintain financial flexibility.

🎯 Putting Qt to Work: Assessing and Improving

To assess whether your Qt is appropriate and identify areas for improvement, follow these steps:

Step 1: Accuracy

Ensure the accuracy of the Qt inputs by obtaining an up-to-date net worth statement and accurate spending figures.

Step 2: Assessment

Although it’s vital to understand your Qt individually, it’s best to evaluate all Term scores together to assess your total asset mix holistically.

Step 3: Improvement

To enhance your Qt, consider the following questions:

- What retirement plan options are available to you? For most CRNAs this is likely a 403(b), 401(k), or 403(b)

- Are you maximizing employer benefits?

- Do you have any old plans that can be rolled over?

For CRNAs who are business owners (yes, 1099 CRNAs, I mean you):

- Given your cash flow, and savings rate, is your current retirement plan suitable?

Additionally, assess your liquidity needs and determine if you should prioritize building liquidity or qualified retirement assets. Consider whether contributing more to retirement accounts could reduce your overall tax liability.

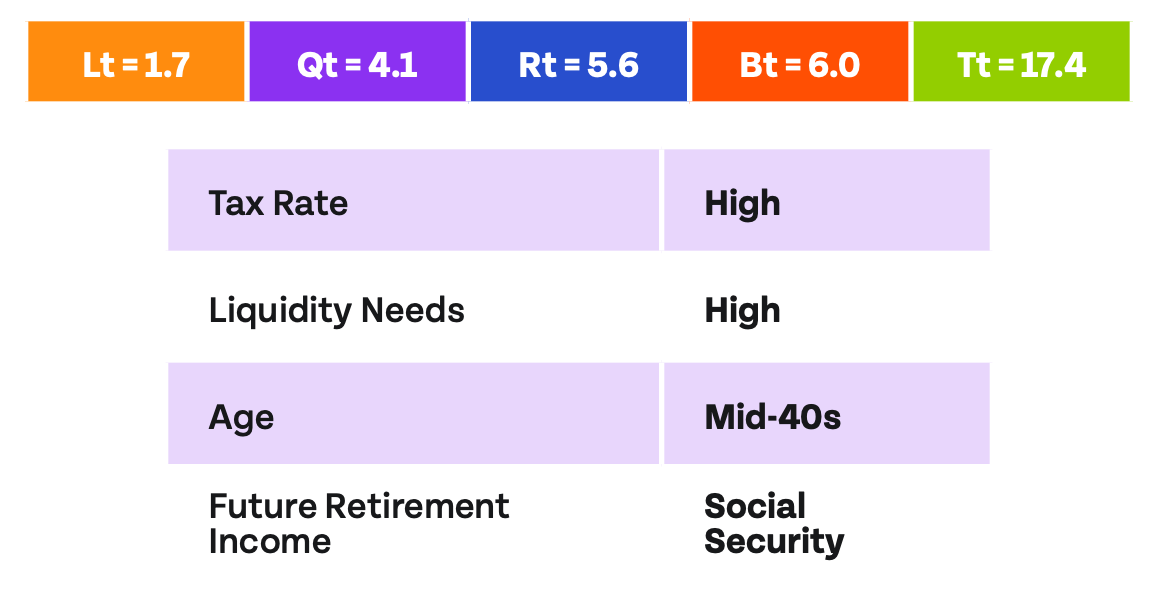

📚 Case Study: A Practical Example

In this case study, we’ll apply the principles outlined above, assuming you have already ensured a good estimate of your Qt.

Score Assessment:

Considering the high tax rate, you might initially think your Qt is low, as a higher tax rate generally necessitates higher pre-tax contributions. However, considering your high liquidity needs, allocating some cash flow toward increasing your Liquid Term also makes sense.

Identify Improvements:

Begin by focusing on improving your Savings Rate to increase both your Liquid Term and Qualified Term. After that, aim to build your after-tax and pre-tax investments equally. This approach allows you to reduce tax liability and build liquidity simultaneously.

💪 Strengthen Your Financial Future

Understanding your Qt and its impact factors is crucial for optimizing your financial health and ensuring a secure retirement. By closely monitoring your Qualified Term and adjusting as needed, you’ll be better equipped to strike the ideal balance between retirement and liquid accounts. This, in turn, will help you achieve your financial goals and enjoy a comfortable lifestyle in the long run.

As always – stay on point!